How to Prepare?

Have you ever gone shopping without your wallet? You find the perfect thing, but by the time you go home for your wallet and come back, someone else will buy it because they planned ahead. This is why the first step in home buying is to get your financial ducks in a row. You will need proof of funds or a lender letter before any decent agent will take you house hunting.

Before you start shopping, it’s a good idea to:

- Set a budget (a mortgage broker can help with this)

- Plan for a down payment (typically between 10 and 20 percent of the asking price)

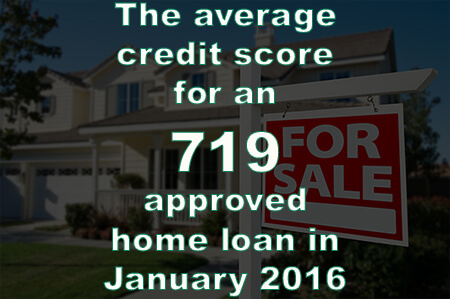

- Get copies of your current credit report

- Become an optimal credit candidate

- Get preapproved for a home loan

What Will a Lender Require?

To get preapproved for a mortgage, you’ll want to meet with a mortgage broker or lender, who will assess your credit and finances to determine whether you are “mortgage-ready”. Getting a preapproval letter can give you buying power when you’re shopping around, since sellers may prefer to contract with a buyer who has already qualified for a mortgage.

NOTE: A prequalification letter is NOT the same as a preapproval. The prequalification basically means that a lender has checked your credit, but this does NOT mean you will be approved for a home loan. Preapproval or “approval letter” means your lender has examined your qualifications and determined that you will be able to obtain a home loan, provided your financial situation remains the same throughout the home buying process. To get preapproved, your lender will request: